Food delivery platforms only recorded a 5% growth in 2023. (Image by Shutterstock).

The future of food delivery platforms in SEA

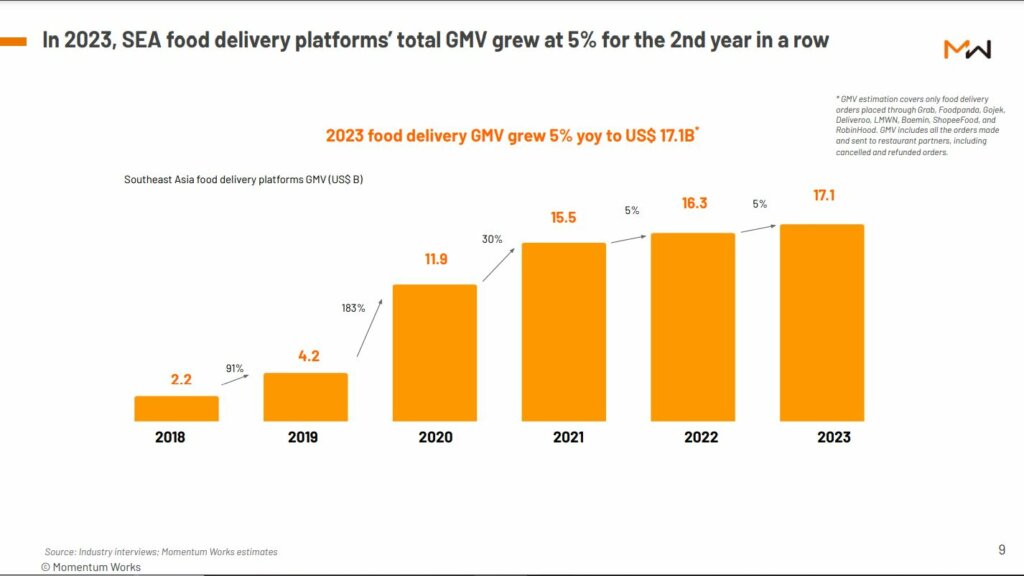

- Food delivery platforms grew 5% in 2023.

- Vietnam’s led the region’s food delivery growth.

- Consolidations in the industry to continue in 2024.

Food delivery platforms have been one of the most successful businesses since the Covid-19 pandemic. While other businesses tried to remain profitable by moving their operations online, their success was nowhere near what food delivery platforms were achieving.

According to a new study by Momentum Works, Southeast Asia’s total food delivery spending on platforms grew a modest 5% to reach US$17.1 billion in 2023. As the growth slows down in the post-pandemic era, the industry is now looking at how it can remain profitable, with mergers and consolidations on the cards for some food delivery platforms.

As expected, Singapore’s Grab remains the market leader in the region with a 55% GMW. A distant second is Foodpanda at 15.8% while Gojek comes in third at 10.5%. Both ShopeeFood and Line Man also showed notable growth in the region.

Despite Grab being the market leader, Singapore did not lead the growth of food delivery platforms. That was Vietnam, which grew by almost 30.0% despite cost control from almost all food delivery players. Vietnam is considered to be the region’s smallest food delivery market.

“Grab continues to gain significant market share in Singapore, Malaysia and the Philippines, as well as in Indonesia – the region’s largest market. ShopeeFood, which has received little attention from outside because of the larger e-commerce battle Shopee is fighting, actually grew the most (almost ⅔); while Line Man in Thailand also recorded double-digit growth,” the report stated.

Vietnam led the region’s food delivery growth in 2023. (Source – Momentum Works).

In terms of spending, total F&B spending in Southeast Asia is estimated to have been US$125.2 billion in 2023, surpassing pre-pandemic levels, however, premium F&B brands (notably in Singapore) face challenges. Many premium brands in Singapore found the year tougher than 2022, with many resorting to cost-cutting measures amid macro uncertainties and inflation. This may have heightened price sensitivity among middle-class diners.

The year 2023 also saw an acceleration of Chinese F&B brands’ entry and expansion into Southeast Asia. This trend is exemplified by Luckin Coffee’s 30 stores in Singapore and Mixue’s close to 4000 outlets across Southeast Asia. Brands in multiple categories and sizes have also established a presence in the region. They have brought in their know-how in in-store operations, marketing, user operations and franchise management. This momentum is expected to increase more in 2024.

Consolidation of food delivery platforms

In 2023, consolidation headlined some food delivery operators. Apart from a few smaller food delivery platforms shutting down their businesses, some are choosing to merge and consolidate their business.

Most major platforms have either achieved or are on track to attain adjusted EBITDA breakeven, with some targeting positive free cash flow in 2024. But, as Meituan and Uber experiences have shown, profitability might not be a constant state – platforms need to constantly balance growth with sustained profitability.

For example, AirAsia consolidated its food delivery business with Foodpanda last year. But that was just the beginning of a bigger consolidation process. According to reports, DeliveryHero is planning to divest Foodpanda. And Grab may be looking to pounce on this opportunity to become the dominant food delivery platform in the region.

“With robust F&B consumption, low food delivery penetration and ongoing consolidation, there is a lot of room for growth for food delivery platforms in the region. While focusing on their core capabilities, leading players also need to keep an eye on potential market changes and emerging challengers,” said Jianggan Li, chief executive officer and Founder of Momentum Works.

Southeast Asia’s leading player Grab only has 5% of the region’s population of 600 million as monthly transacting customers. (Image by Shutterstock).

In terms of business strategy, food delivery players are now using advertising for revenue expansion such as advertising products to lock in more merchant investments. Platforms are expanding their advertising product portfolios to cater to the distinct needs of various brands, including large F&B chains, small F&B merchants, and FMCG brands.

Southeast Asia’s leading player Grab only has 5% of the region’s population of 600 million as monthly transacting customers. Amid a flat sector topline, untapped populations in major cities, expansion into smaller cities, and catering to tourists present further growth opportunities for food delivery platforms. Platforms can and should also continuously optimize operations to reduce costs and grow their bottom line.

At the same time, as the Indonesia-focused Gojek declines slightly, the recent Tokopedia-TikTok Shop Indonesia merger opens up two possible scenarios for the industry. First, there could be more resources for Gojek since GoTo Group has jettisoned the significantly loss-making e-commerce arm or second, GoTo Group will further re-examine its strategy and re-open consolidation talks with Grab.

Either way, 2024 seems to be a promising year for Grab in the food delivery platform arena For other players, it is all about how they play their cards and hope to remain profitable with the growing competition in the industry.

This was a year ago – so what does the future look like for Grab and others?

READ MORE

- Safer Automation: How Sophic and Firmus Succeeded in Malaysia with MDEC’s Support

- Privilege granted, not gained: Intelligent authorization for enhanced infrastructure productivity

- Low-Code produces the Proof-of-Possibilities

- New Wearables Enable Staff to Work Faster and Safer

- Experts weigh in on Oracle’s departure from adland