What is embedded finance – and why is it the all-round payments game-changer?

Spurred on by shifting consumer expectations for seamless digital customer journeys, embedded finance has moved from a nice-to-have addition to one of the critical additions to the fintech space in recent years.

The common-sense pragmatism and outright convenience of embedded finance options will revolutionize B2B and B2C payments, not to mention digitalizing a host of financial services that used to be the domain of traditional banks and financial institutions.

But since the advent of open banking (where interoperability between third-party financial service providers and the classical banking sector is enabled via APIs), disruptive fintech game-changers have capitalized on market demand for interconnectivity between payment methods, cashless payments, and transactions not limited by geography or different currencies.

The capabilities of embedded finance in filling several gaps in the current financial ecosystem are game-changing in more ways than one. Before now, most companies did not have the expertise to develop their digital financial products. Before the pandemic, especially in Asia Pacific (APAC), where the region is huge and without standardized compliance processes, and financial inclusion is traditionally low, many organizations did not see the benefits of investing significant time and resources into their solutions.

Compliance and anti-money laundering (AML) regulations are of paramount importance, as they involve handling personal and organizations’ money and sensitive data. Introducing new, disruptive services into a tightly regulated space has drawbacks. Service providers must ensure they meet the regulatory requirements of different regions and industries to be trusted and widely accepted.

With APIs and Software-as-a-Service (SaaS) ensuring easy access and integration with different applications, environments, and tools, embedded finance is becoming the fintech solution of choice for all industries, especially after realizing that their prior business models were not delivering a great customer experience.

By embracing embedded finance, businesses can level up their digital offerings in more ways than just accepting cashless payments. Digital-first and digital-only outfits can extend their services using methods formerly reserved for traditional FSI (financial services industry), such as microloans, wealth management, buy now pay later, insurance, and electronic invoicing.

E-commerce supplier Shopify.com enables smaller merchants to set up their online stores on its platform. To support a streamlined financial ecosystem across all its merchants, Shopify leverages a white-label solution from Stripe, making all payment options available to all merchant microsites. Each merchant can customize their store, so the user experience is bespoke – but with standardized underlying support, the complexities of PCI compliance, security, and payments integration are handled.

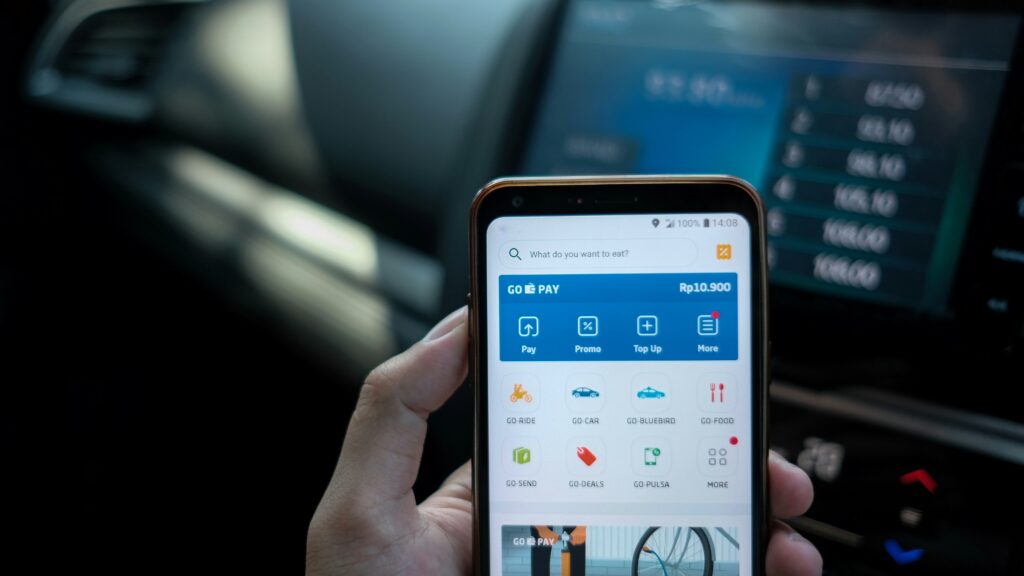

Photo by Edi Kurniawan on Unsplash

Grab, the popular Southeast Asian (SEA) super app that started as a ride-hailing service, offers a range of embedded finance options over its base payment environment, offering financial services like buy now pay later credit facilities, auto insurance deductions for late deliveries and rides, payment types from various service providers, and even investment opportunities.

TazaPay.com offers secure escrow services for customers to address the online shopping problem posed by customers wanting to see products before paying and merchants wanting to receive monies before releasing the product. TazaPay does away with the middleman of a trusted intermediate platform like Amazon, Taobao, or Carousell, allowing direct interchange between sellers and buyers via escrow services.

In the traditional FSI, legacy infrastructure, complex compliance, and other fiscally responsible requirements mean the sector has been slow to grasp emerging digital offerings, often opting for one-off in-house development of new features; costly compared to an integrated embedded finance solution.

But just as financial institutes embraced the advantages of open banking, the agility and scalability of embedded finance options mean that banks can adapt these fintech solutions alongside their existing front-ends at a fraction of the cost compared to the R&D time, work hours, and integration costs associated with their existing infrastructures.

At the forefront of this financial revolution is Currencycloud, whose tech allows industries to embed finance into the core of their business. Digital wallets and frictionless cross-border transactions can be placed without re-engineering legacy tech stacks.

Currencycloud is democratizing finance by expanding the embedded finance market to technology companies and organizations with global aspirations, not just so-called ‘disruptors’. Currencycloud is well-equipped to help financial services companies transform into digital businesses. It powers cross-border money movements and simplifies collection, conversion, and payments processes.

To find out how to supercharge your company’s B2B and B2C financial services, get in touch with Currencycloud today.

READ MORE

- Strategies for Democratizing GenAI

- The criticality of endpoint management in cybersecurity and operations

- Ethical AI: The renewed importance of safeguarding data and customer privacy in Generative AI applications

- How Japan balances AI-driven opportunities with cybersecurity needs

- Deploying SASE: Benchmarking your approach